August 2015 NASDAQ: WHLR Exhibit 99.1 |

| August 2015 NASDAQ: WHLR Exhibit 99.1 |

2 SAFE HARBOR Wheeler Real Estate Investment Trust, Inc. (the “Company”) considers portions of the information in this presentation to be forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, both as amended, with respect to the Company's expectation for future periods. Although the Company believes that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, it can give no assurance that its expectations will be achieved. For this purpose, any statements contained herein that are not historical fact may be deemed to be forward-looking statements. There are a number of important factors that could cause results to differ materially from those indicated by such forward-looking statements, including, among other factors, local conditions such as oversupply of space or a reduction in demand for real estate in the area; competition from other available space; dependence on rental income from real property; the loss of, significant downsizing of or bankruptcy of a major tenant; constructing properties or expansions that produce a desired yield on investment; the Company’s ability to renew or enter into new leases at favorable rates; to buy or sell assets on commercially reasonable terms; to complete acquisitions or dispositions of assets under contract, to secure equity or debt financing on commercially acceptable terms or at all; to enter into definitive agreements with regard to financing and joint venture arrangements or the Company’s failure to satisfy conditions to the completion of these arrangements. For additional factors that could cause the results of the Company to differ materially from those indicated in the forward-looking statements, please refer to “Risk Factors” listed in the Company’s most annual report filed with the SEC and available for review at www.sec.gov. Readers are cautioned that forward looking statements are not guarantees of future performance, and should not place undue reliance on them. In formulating the forward looking statements contained in this presentation, it has been assumed that business and economic conditions affecting Wheeler will continue substantially in the ordinary course. These assumptions, although considered reasonable at the time of preparation, may prove to be incorrect. |

3 COMPANY OVERVIEW Wheeler is an internally-managed REIT focused on acquiring well-located, necessity-based retail properties Target grocery-anchored shopping centers in secondary and tertiary markets with strong demographics Acquire properties at attractive yields and significant discount to replacement cost Current portfolio of 48 properties with approximately 2.7 million square feet of Gross Leasable Area 38 shopping center/retail properties, 8 undeveloped land parcels, 1 redevelopment property and 1 self- occupied office building Approximately 90% of centers are anchored or shadow-anchored by a grocery store Dedicated management team with strong track record of acquiring and selling retail properties through multiple phases of the investment cycle Predecessor firm achieved an average IRR of approximately 28% on 11 dispositions Wheeler Real Estate Investment Trust Exchange: Nasdaq Ticker: WHLR Market Cap (1) : $125.9 million Stock Price (1) : $1.91 52-Week Trading Range: $1.85-$5.15 Common Stock Outstanding: 65.9 million Annualized Dividend: $0. 21 Dividend Yield (1) : 11.0% 1) As of 8/11/2015 Butler Square |

4 Industry leading occupancy rate of approximately 94.5% * National and Regional merchants represent majority of Wheeler’s tenants

Diversified geography and tenant base

INVESTMENT HIGHLIGHTS

High Quality Existing

Portfolio Wheeler properties serve the essential day-to-day shopping needs of the surrounding

communities

Majority of tenants provide non-cyclical consumer goods and

services that are less impacted by fluctuations in the

economy Necessity-Based

Retail Secondary and Tertiary markets have limited competition from institutional buyers and low

levels of new construction

Target markets experiencing selling pressure from generational

transition, larger REITs shifting to core markets and

expiring CMBS debt Attractive Niche

Market Opportunity

Ability to scale platform as the Company grows results in improved

profitability Create value through intensive leasing and

property expense management Deep retailer relationships

provide unique market knowledge Third-party property

management and development fees create additional revenue stream Internally-Managed, Scalable Platform * As of 8/11/2015 |

5 Steven M. Belote Chief Financial Officer Wheeler’s Chief Financial Officer since 2011 Prior to joining Wheeler, worked at Shore Bank, as their CFO, playing a significant role in IPO during 1997 Previous experience also includes seven years at BDO Seidman, LLP, a large international public accounting and consulting firm Jon S. Wheeler Chairman and CEO Over 33 years of experience in the real estate industry In 1999, founded Wheeler Interests, LLC (“Wheeler Interests”), a company which we consider our predecessor firm, that focuses on the acquisition, leasing, management, renovation & development of commercial shopping center properties Overseen the acquisition of over 60 properties with Wheeler Interests WHLR’s executive officers, together with the management teams of its service companies,

have an aggregate of over 150 years of experience in the real estate

industry. SEASONED, ACCOMPLISHED & REPUTABLE

MANAGEMENT TEAM Dave Kelly

SVP, Director of Acquisitions

Over 25 years of experience in the real estate industry Previously served 13 years as Director of Real Estate for Supervalu, Inc., a Fortune 100 supermarket retailer Focused on site selection and acquisition for Supervalu from New England to the Carolinas completing transactions totaling over $500 million Jeff Parker Director of Leasing Recently joined Wheeler and is responsible for overseeing all leasing operations of the portfolio Previously served as Real Estate Portfolio Manager for Southeast and Mid-Atlantic regions for Dollar Tree Prior to Dollar Tree, Mr. Parker spent ten years handling the leasing and sale of commercial properties at CB Richard Ellis, Inc. |

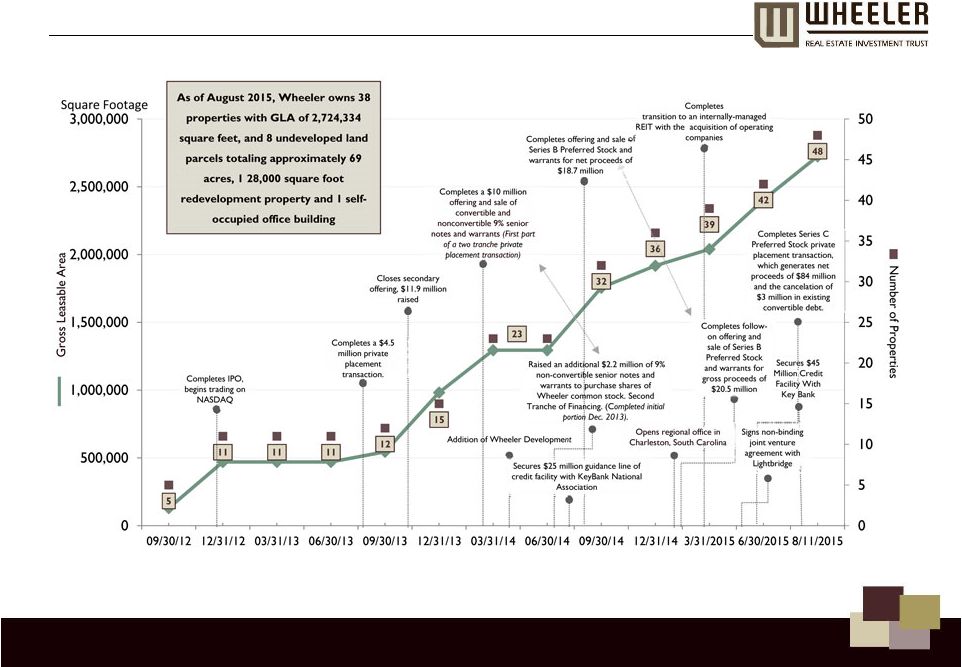

6 GROWTH STORY |

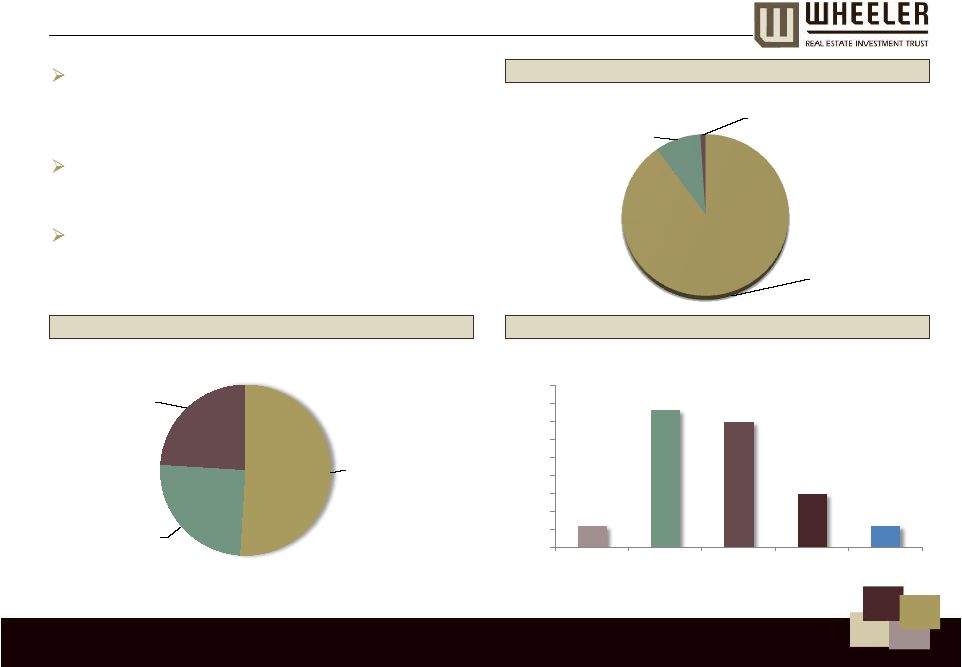

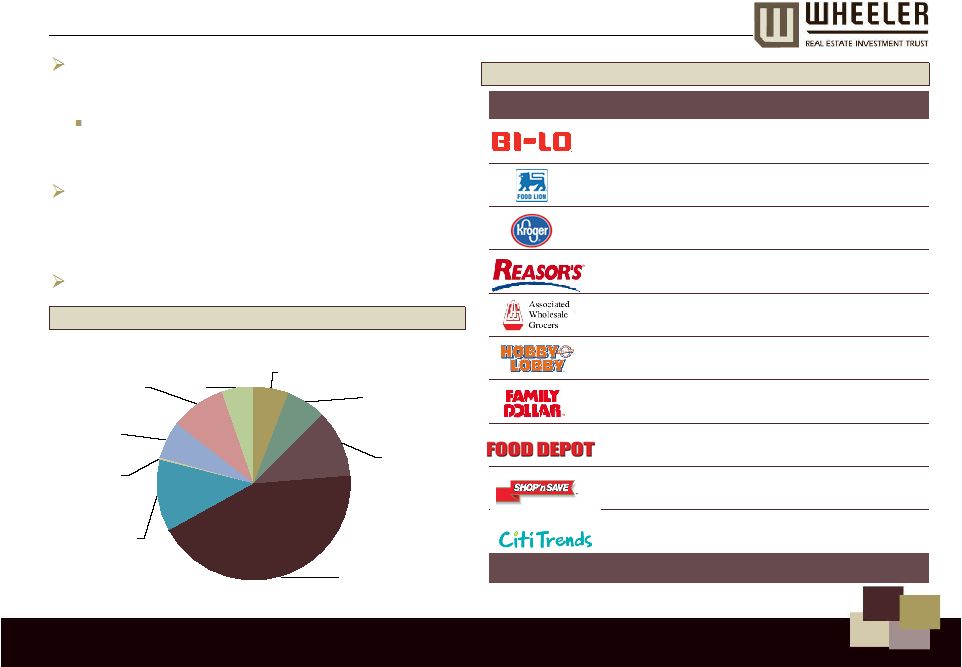

7 STABLE PORTFOLIO FOCUSED ON NECESSITY-BASED SHOPPING Predominantly Grocery-Anchored Portfolio 2 Strong Grocer Rent to Sales 3 Grocery- Anchored 90% Non- Grocery/ Community Center 9% Free- standing retail 1% 6% 38% 35% 15% 6% 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% < 1.0% 1.0% to 2.0% 2.0% to 3.0% 3.0% to 4.0% 4.0%+ 79% of grocery store GLA with a rent/sales ratio below 3% Company believes necessity-based shopping centers are resistant to economic downturns. In our view, Necessity = Stability The average consumer in the US makes a trip to a grocery store 2.2 times per week 1 During 2009-2014, US grocer sales increased 24%, demonstrating strength of the traditional grocery store 1 Strong National and Regional Tenants National 51% Regional 25% Local 24% 82% of Wheeler's GLA is occupied by national & regional tenants

1) Source: Food Marketing Institute. 2) Based on percentage of GLA with a grocery store included in the shopping center or as a shadow-anchor. 3) Based on 2014 sales from 19 grocers who report sales to us in our current portfolio. |

8 Type GLA % of GLA Grocery 265,391 11.04% Grocery 191,280 7.96% Grocery 84,938 3.53% Grocery 81,000 3.37% Grocery 75,000 3.12% Home Goods 58,935 2.45% Grocery 58,473 2.43% Grocery 57,427 2.39% Grocery 46,700 1.94% Grocery 37,500 1.56% Total 956,644 39.79% Restaurant 5.8% Services 6.7% Health & personal care 11.2% Grocery 43.2% Apparel & Accessories 12.0% Electronics 0.40% Home 6.2% General Merchandise 9.2% Other 5.3% TENANT OVERVIEW Top 10 Tenants 1 Top tenants represent approximately 40% of portfolio Tenant concentration expected to be reduced significantly after offering proceeds deployed Focus on tenants that create consistent consumer demand offering items such as food, postal, dry- cleaning, health services and discount merchandise Minimal exposure to E-Commerce industry 1) As of 6/30/2015 Diversified Merchandise Mix 1 |

9 LEASE EXPIRATION SCHEDULE 1 Approximately 83% of GLA leased through 2016 or beyond Weighted average remaining lease term of 4.91 years Weighted average remaining lease term for grocery anchor tenants is 6.54 years 6.02% 10.92% 11.09% 20.42% 12.28% 39.27% 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% 35.00% 40.00% 45.00% 2015 2016 2017 2018 2019 2020+ % of Total Gross Leasable Area Expiring 1 1) As of 6/30/2015 |

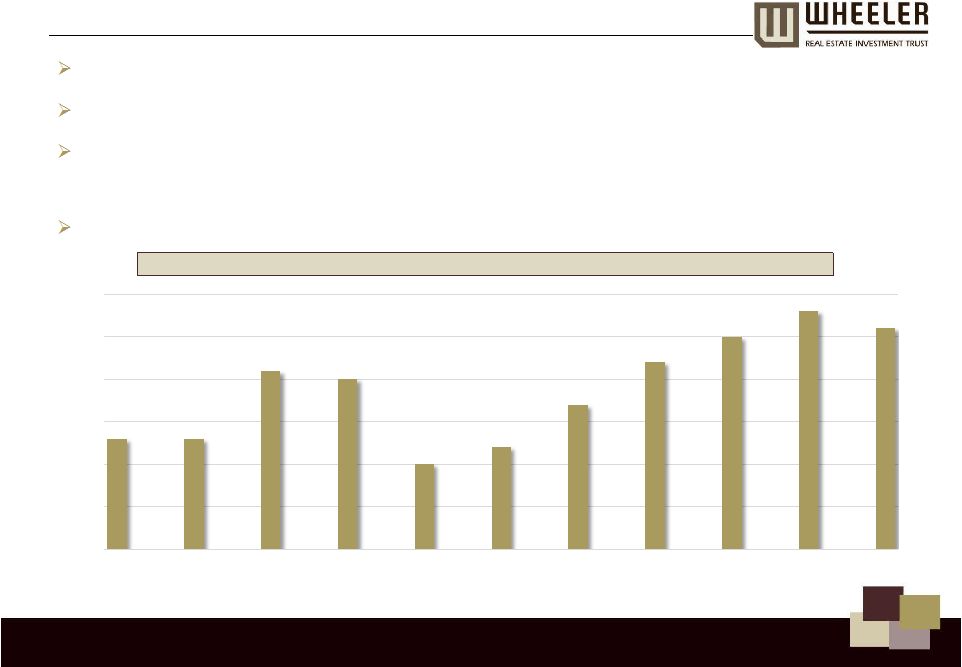

10 STRONG LEASING TRENDS Wheeler has maintained stable occupancy rates – average of 94.9% since the Company’s IPO 33 renewals in 2014 resulted in a weighted average increase of 6.6% in base rent For the first six months of 2015, approximately 155,963 square feet was renewed at a average weighted increase of 7.24% Industry average occupancy rate across sectors of REITs is measured at 93.6% 1 Historical Occupancy Rates 94.3% 94.3% 95.1% 95.0% 94.0% 94.2% 94.7% 95.2% 95.5% 95.8% 95.6% 93.0% 93.5% 94.0% 94.5% 95.0% 95.5% 96.0% Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 1) Source: Investment News. |

11 INTEGRATED PLATFORM, PROVEN SUCCESS Wheeler has acquisition, leasing, property management, development and re-development services all in–house Over 50 associates Since the acquisition of Wheeler Development in January 2014, Wheeler has acquired seven undeveloped properties totaling approximately 67 acres of land and one redevelopment property. Development and leasing services generate significant fees from third-party contracts Extensive pipeline of third-party projects expected to break ground in 2015 and 2016 Company anticipates by year-end 2015, it will report approximately $375,000 in third party development fees and $530,000 in external leasing commissions Predecessor development segment developed nine properties in four states – seven are currently owned by Wheeler Asset Management Acquisitions & Development Leasing & Business Dev. The Shoppes at Eagle Harbor Developed by Wheeler Development in 2009 Corporate & Accounting |

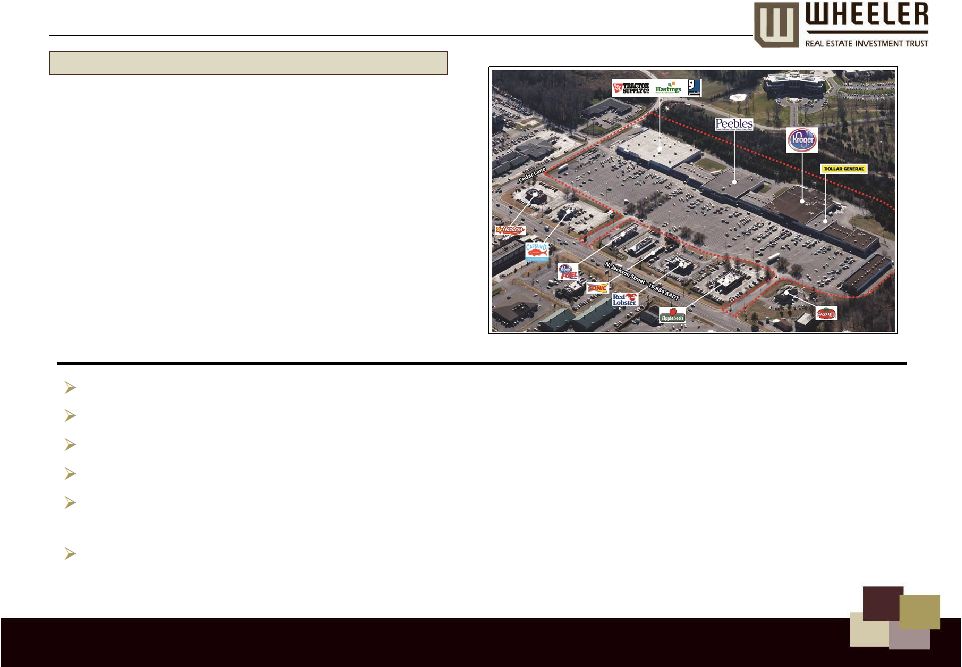

12 CASE STUDY: FORREST GALLERY - TULLAHOMA, TN Purchase Price LTV Square Feet Price / Foot Anchor Occupancy Acquisition Cap Rate Cost of Debt Estimated ROE Built $11,500,000 79% 214,451 $54 Kroger 92% 8.8% 5.4% 21.6% 1987 Third-party property purchased in 2013 Tullahoma is ranked as the #1 “micropolitan” city in the state of Tennessee based on economic strength

Strong frontage on the main street in Tullahoma has drawn multiple

popular restaurants and retailers In discussion with Kroger

to expand at their expense and relocate Dollar General to parking lot out-parcel Recent Improvements include new roof on Kroger and out parcel which will be 100% recaptured through

CAM Peebles recently exercised two 5-year options to extend lease to 2026

1) Number one ranked in 2014 and 2013 by Policom based on economic strength factors such as employment, earnings, cost of living and standard of living. Investment Summary |

13 GROWTH STRATEGY Well located properties in secondary and tertiary markets High unlevered returns (expected cap rates of ~9%) Focus on best in market grocery-anchored centers with necessity-based inline tenants National & regional tenants High traffic count and ease of access Ancillary & Specialty Income Opportunity to improve revenue through active lease and expense management Utilizing exterior parking for build to suit outparcels or pad sales Maximizing CAM reimbursement income available from existing leases Company utilizes strict underwriting guidelines and unique due diligence processes to identify key issues and uncover hidden opportunities with large potential upside |

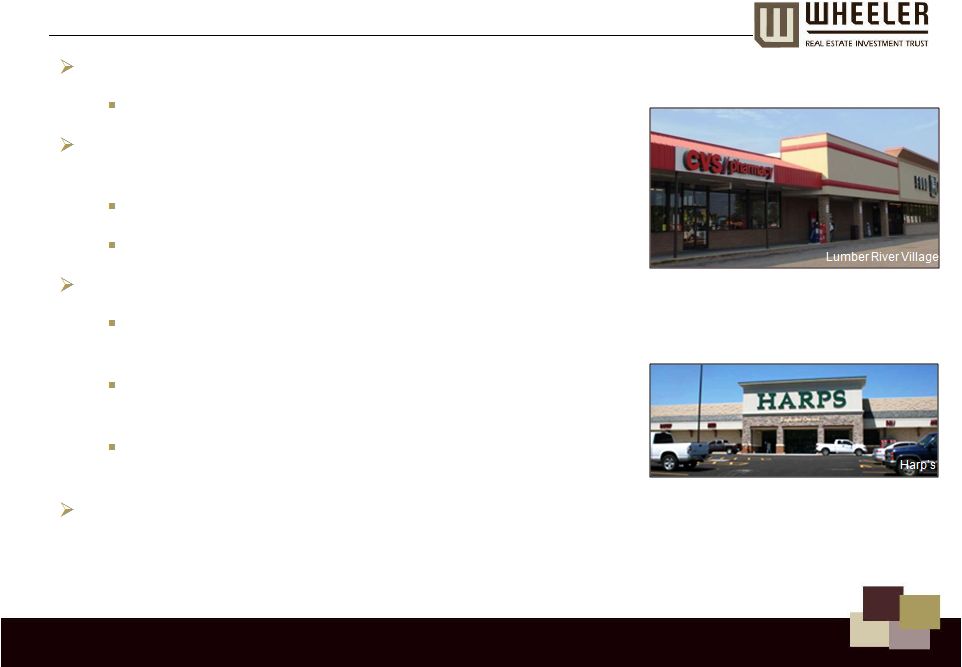

14 ACQUISITION UPDATE Year to date, the Company has closed on eight shopping center properties: Alex City Marketplace, Butler Square, Brook Run, Beaver Ruin I, Beaver Ruin II, Chesapeake Square, Pierpont Center and Sunshine Plaza for a total acquisition value of approximately $85.4 million with an average cap rate of 8.76%; an average interest rate of 4.25%; and, LTV of 56% In 2015, the Company acquired 3 raw land parcels totaling 4.5 acres and Columbia Fire Station, a 28,000 square foot redevelopment property. 24 properties (individual sales and 2 property portfolios) under LOI or contract requiring equity investment of $71.4 million at average cap rate of 8.79% with in place leases Anticipate financing with 55% LTV at approximately 4.5% At any given time, the Company is typically evaluating properties or negotiating LOI’s with total value of $75 -$100 million Beaver Ruin Village |

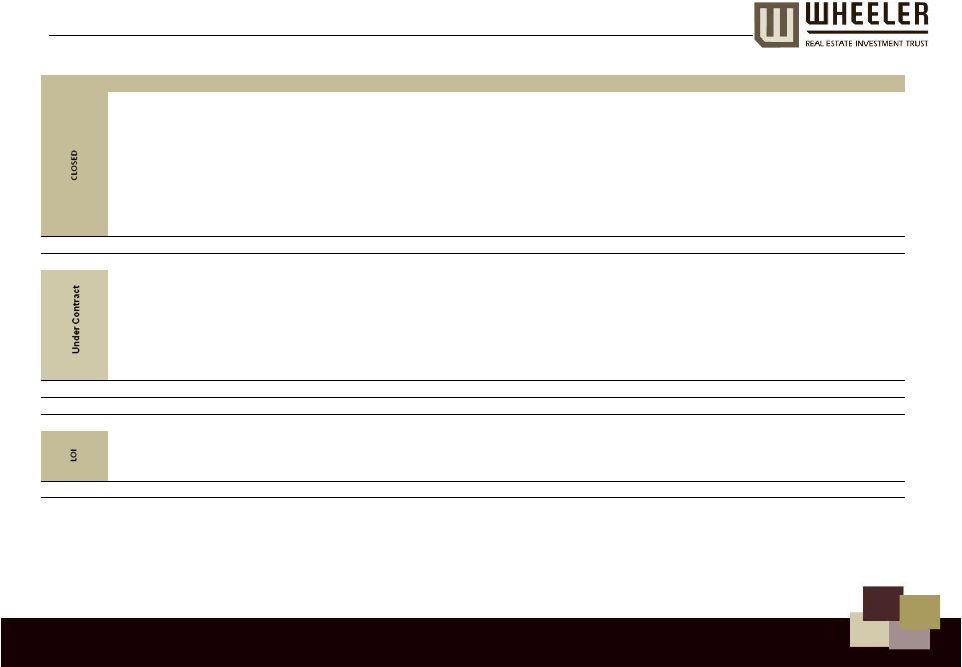

15 CURRENT PIPELINE (as of 8/11/2015) Status Property Name Location Square Footage Anchor Price Cap Interest Rate LTV Pierpont Center Morgantown, WV 122,259 Shop n Save $ 13,885,000 9.23% 4.15% 70.58% Alex Marketplace Alexander City, AL 147,791 Winn Dixie $ 10,250,000 8.99% 3.95% 56.10% Butler Square Mauldin, SC 82,400 Bi Lo $ 9,400,000 8.60% 3.90% 60.00% Brook Run Richmond, VA 147,738 Martin's $ 18,500,000 8.12% 4.08% 59.19% Beaver Ruin Village Lilburn, GA 74,038 Kroger (Shadow) $ 12,350,000 8.58% 4.73% 56.68% Beaver Ruin Village II Lilburn, GA 34,925 Advanced Auto $ 4,375,000 9.03% 4.73% 54.86% Chesapeake Square Onley, VA 99,848 Food Lion $ 6,340,000 10.01% - 0.00% Sunshine Plaza Lehigh Acres, FL 111,189 Winn Dixie, Ace Hardware $ 10,350,000 8.56% 4.57% 57.00% Total Closed 820,188 $ 85,450,000 8.76% 4.25% 55.52% Barnett Portfolio (3) North Carolina 171,370 Food Lion (3) $ 15,325,000 8.78% TBD 57% Grove Park South Carolina 106,557 BiLo $ 6,600,000 8.95% TBD 58% Conyers Crossing Georgia 170,475 Hobby Lobby $ 10,750,000 8.90% TBD 55% Parkway Plaza Georgia 52,365 Winn Dixie $ 6,075,000 8.55% TBD 58% Fort Howard Square Georgia 113,652 Goody's, Goodwill, Fred's $ 11,500,000 8.89% TBD 55% SC Shopping Center South Carolina 61,335 BiLo $ 7,000,000 8.90% TBD 57% Total Contract 675,754 $ 57,250,000 8.83% 57% Closed and Contract 1,495,942 $ 142,700,000 8.79% 56% SC Shopping Center South Carolina 26,103 Walmart (Shadow) $ 5,100,000 8.81% 57% SC Portfolio (14) South Carolina 603,142 Various $ 72,500,000 8.97% 55% SC Shopping Center South Carolina 181,457 Grocery $ 20,500,000 8.09% 55% Total LOI 810,702 $ 98,100,000 8.78% 55% Total All Categories 2,306,644 $ 240,800,000 8.79% 56% |

16 INVESTMENT HIGHLIGHTS Necessity-based Retail High Quality Existing Portfolio Attractive Niche Market Opportunity Internally-Managed, Scalable Platform |

Appendix |

18 PROPERTY OVERVIEW (as of 8/11/2015) Property Location Number of Tenants Net Leasable Square Feet Total Square Feet Leased Percentage Leased Annualized Base Rent Annualized Base Rent per Leased Square Foot Alex City Marketplace Alexander City, AL 17 147,791 127,141 86.03% $ 951,791 $ 7.49 Amscot Building Tampa, FL 1 2,500 2,500 100.00% 100,738 40.30 Beaver Ruin Village Lilburn, GA 29 74,038 67,763 91.52% 1,072,234 15.82 Beaver Ruin Village II Lilburn, GA 4 34,925 34,925 100.00% 404,092 11.57 Berkley (2) Norfolk, VA - - - - - - Bixby Commons Bixby, OK 75,000 75,000 100.00% 768,500 10.25 Brook Run Properties (2) Richmond, VA - - - - - - Brook Run Shopping Center Richmond, VA 18 147,738 134,791 91.24% 1,584,179 11.75 Bryan Station Lexington, KY 9 54,397 54,397 100.00% 553,008 10.17 Butler Square Mauldin, South Carolina 16 82,400 82,400 100.00% 851,795 10.34 Carolina Place (2) Onley, VA - - - - - - Chesapeake Square Onley, VA 10 99,848 76,048 76.16% 607,583 7.99 Clover Plaza Clover, SC 10 45,575 45,575 100.00% 349,843 7.68 Columbia Station (2) Columbia, SC - - - - - - Courtland Commons (2) Courtland, VA - - - - - - Crockett Square Morristown, TN 4 107,122 107,122 100.00% 871,897 8.14 Cypress Shopping Center Boiling Springs, SC 13 80,435 73,785 91.73% 755,162 10.23 Edenton Commons (2) Edenton, NC - - - - - - Forrest Gallery Tullahoma, TN 26 214,451 199,816 93.18% 1,181,234 5.91 Freeway Junction Stockbridge, GA 17 156,834 153,299 97.75% 1,010,753 6.59 Graystone Crossing Tega Cay, SC 11 21,997 21,997 100.00% 504,443 22.93 Harbor Point (2) Grove, OK - - - - - - Harps at Harbor Point Grove, OK 1 31,500 31,500 100.00% 364,432 11.57 Harrodsburg Marketplace Harrodsburg, KY 8 60,048 58,248 97.00% 438,556 7.53 Jenks Plaza Jenks, OK 5 7,800 7,800 100.00% 143,416 18.39 Jenks Reasors Jenks, OK 1 81,000 81,000 100.00% 912,000 11.26 LaGrange Marketplace LaGrange, GA 13 76,594 71,494 93.34% 385,317 5.39 Laskin Road (2) Virginia Beach, VA - - - - - - Lumber River Village Lumberton, NC 12 66,781 66,781 100.00% 497,490 7.45 Monarch Bank Virginia Beach, VA 1 3,620 3,620 100.00% 250,538 69.21 Perimeter Square Tulsa, OK 8 58,277 55,773 95.70% 677,789 12.15 Pierpont Centre Morgantown, WV 20 122,259 122,259 100.00% 1,327,437 10.86 Port Crossing Harrisonburg, VA 7 65,365 57,710 88.29% 737,392 12.78 Riversedge North (1) Virginia Beach, VA - - - 0.00% - - Shoppes at TJ Maxx Richmond, VA 16 93,552 90,539 96.78% 1,062,636 11.74 South Square Lancaster, SC 5 44,350 39,850 89.85% 318,822 8.00 Starbucks/Verizon Virginia Beach, VA 2 5,600 5,600 100.00% 185,695 33.16 St. George Plaza St. George, SC 6 59,279 50,829 85.75% 357,393 7.03 Sunshine Shopping Plaza Lehigh Acres, FL 21 111,189 107,486 96.67% 948,880 8.83 Surrey Plaza Hawkinsville, GA 5 42,680 42,680 100.00% 291,495 6.83 Tampa Festival Tampa, FL 22 137,987 137,987 100.00% 1,224,828 8.88 The Shoppes at Eagle Harbor Carrollton, VA 7 23,303 23,303 100.00% 454,530 19.51 Tulls Creek (2) Moyock, NC - - - - - - Twin City Commons Batesburg-Leesville, SC 5 47,680 47,680 100.00% 449,194 9.42 Walnut Hill Plaza Petersburg, VA 11 87,239 74,345 85.22% 593,323 7.98 Waterway Plaza Little River, SC 8 49,750 46,150 92.76% 396,983 8.60 Westland Square West Columbia, SC 9 62,735 58,365 93.03% 435,311 7.46 Winslow Plaza Sicklerville, NJ 14 40,695 37,095 91.15% 526,530 14.19 Total Portfolio 393 2,724,334 2,574,653 94.51% $ 24,547,239 $ 9.53 1) Riversedge North is Company’s corporate office. 2) Undeveloped/redevelopment property |

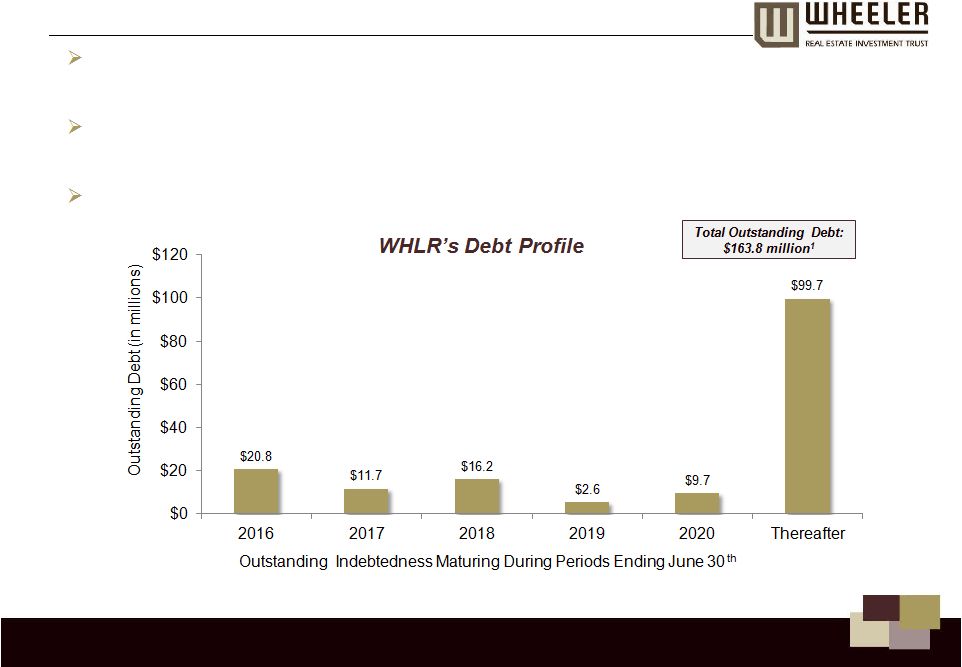

19 Strong lending relationships with nationally recognized banks; strong capital position expected to significantly improve bargaining power Recently expanded revolving credit facility with KeyBank National Association for $45 million with an accordion feature for up to $100 million Weighted average interest rate of 4.86% DEBT / MATURITY PROFILE 1 1) As of 6/30/2015 |

CONSOLIDATED STATEMENT OF OPERATIONS 20 Three Months Ended June 30, Six Months Ended June 30, 2015 2014 2015 2014 (unaudited) TOTAL REVENUES 6,703,361 $ 3,633,694 $ 12,455,502 $ 7,297,846 OPERATING EXPENSES: Property operations 1,901,313 909,037 3,533,492 1,832,219 Non-REIT management and leasing services 231,777 — 601,552 — Depreciation and amortization 4,074,749 1,735,944 7,311,233 3,521,546 Provision for credit losses 54,538 (28,032 101,736 (28,032 Corporate general & administrative 3,518,630 1,385,549 5,829,860 2,217,867 Total Operating Expenses 9,781,007 4,002,498 17,377,873 7,543,600 Operating Income (3,077,646) (368,804 (4,922,371 (245,754 Interest expense (2,217,592) (1,536,637 (4,596,056 (2,905,575 Net Loss (5,295,238) (1,905,441 (9,518,427 (3,151,329 Less: Net loss attributable to noncontrolling interests (440,216) (81,451 (902,592 (168,703 Net Loss Attributable to Wheeler REIT (4,855,022) (1,823,990 (8,615,835 (2,982,626 Preferred stock dividends (8,334,102) (423,555 (10,836,325 (464,258 Deemed dividend related to beneficial conversion feature of preferred stock (59,520,000) — (59,520,000 — Net Loss Attributable to Wheeler REIT Common Shareholders (72,709,124) $ (2,247,545 $ (78,972,160 $ (3,446,884 Loss per share: Basic and Diluted (4.13) $ (0.31 $ (6.20 $ (0.47 Weighted-average number of shares: Basic and Diluted 17,594,873 7,329,788 12,727,710 7,258,068 |

BALANCE SHEET SUMMARY 21 June 30, 2015 December 31, 2014 ASSETS: (unaudited) Investment properties, net $ 192,945,133 152,250,986 Cash and cash equivalents 49,165,844 9,969,748 Rents and other tenant receivables, net 2,193,602 1,985,466 Goodwill 5,485,823 7,004,072 Above market lease intangible, net 5,681,901 4,488,900 Deferred costs and other assets, net 45,688,802 29,272,096 Total Assets $ 301,161,105 204,971,268 LIABILITIES: Loans payable $ 163,826,466 141,450,143 Below market lease intangible, net 5,016,648 5,267,073 Accounts payable, accrued expenses and other liabilities 8,227,725 5,130,625 Total Liabilities 177,070,839 151,847,841 Commitments and contingencies — — EQUITY: Series A preferred stock (no par value, 4,500 shares authorized, 1,809 shares issued and outstanding, respectively)

1,458,050 1,458,050 Series B convertible preferred stock (no par value, 3,000,000 shares authorized, 1,595,900 and 1,648,900 shares

issued and outstanding, respectively)

36,806,496 37,620,254 Common stock ($0.01 par value, 150,000,000 and 75,000,000 shares authorized, 54,419,013 and 7,512,979 shares

issued and outstanding, respectively)

544,190 75,129 Additional paid-in capital 183,834,995 31,077,060 Accumulated deficit (108,544,140) (27,660,234) Total Shareholders’ Equity 114,099,591 42,570,259 Noncontrolling interests 9,990,675 10,553,168 Total Equity 124,090,266 53,123,427 Total Liabilities and Equity $ 301,161,105 204,971,268 |

22 FFO and CORE FFO Three Months Ended June 30, Six Months Ended June 30, 2015 2014 2015 2014 (unaudited) Total FFO (1,220,489) $ (169,497 (2,207,194 370,217 Preferred stock dividends (8,334,102) (423,555 (10,836,325 (464,258 Preferred stock accretion adjustments 5,768,361 67,137 6,979,563 67,137 Total FFO available to common shareholders and common unitholders (3,786,230) (525,915 (6,063,956 (26,904 Acquisition costs 740,223 343,000 1,433,739 400,000 Capital related costs 553,132 — 621,650 — Other non-recurring expenses 327,480 — 416,980 — Share-based compensation 256,300 145,000 301,300 145,000 Straight-line rent (34,824) (49,260 (93,435 (138,109 Loan cost amortization 259,050 187,769 745,248 274,600 Above (below) market lease amortization 213,746 (22,452 409,475 (45,756 Perimeter legal accrual 124,300 — 124,300 — Tenant improvement reserves (63,400) — (122,900 — Recurring capital expenditures (76,100) — (147,500 — Total Core FFO (1,486,323) $ 78,142 (2,375,099 608,831 Weighted Average Common Shares 17,594,873 7,329,788 12,727,710 7,258,068 Weighted Average Common Units 3,695,990 2,008,338 3,618,712 1,935,741 Total Common Shares and Units 21,290,863 9,338,126 16,346,422 9,193,809 FFO per Common Share and Common Units (0.18) $ (0.06 (0.37 — Core FFO per Common Share and Common Units (0.07) $ 0.01 (0.15 0.07 Pro forma Core FFO per Common Share and Common Units (1) 0.02 — 0.04 — (1) Pro forma Core FFO assumes the following transactions had occurred on January 1, 2015: (i) the Pierpont Center, Alex City Marketplace, Butler Square, Brook Run Shopping Center, Beaver Ruin Village, Beaver Ruin Village II, Chesapeake Square acquisitions; the Series C Preferred Stock capital raise and subsequent conversion; and the Series A Preferred Stock and Series B Convertible Preferred Stock exchange offer that closed on July 23, 2015. Additionally, we excluded all non-recurring expenses detailed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in our June 2015 Quarterly Report on Form 10-Q, the Lumber River loan which was paid off on May 1, 2015 and any additional common stock and common units issued during the six months ended June 30, 2015 were outstanding for the entire period. The Pro forma Core FFO is being presented solely for purposes of illustrating the potential impact of these transactions as if they occurred on January 1, 2015, based on information currently available to management, and is not necessarily indicative of what actual results would have been had the transactions referred to above occurred on January 1, 2015. |

23 CAPITAL STRUCTURE March 31, 2015 June 30, 2015 Post Exchange 1 Debt Outstanding ($000) Outstanding ($000) Outstanding ($000) Security Senior Non-Convertible Debt (9% Coupon, Dec-15 / Jan-16 Maturity) 2 $6,160 $6,160 $6,160 Senior Convertible Debt (9% Coupon, Dec-18 Maturity) 3 $3,000 $3,000 $3,000 Property Debt (4.74%/4.56% Weighted Average Coupon, Various Maturities)

$138,474 $154,666 $154,666 Total Debt $147,634 $163,826 $163,826 Equity Shares Outstanding Amount ($000) Shares Outstanding Amount ($000) Shares Outstanding Amount ($000) Security Series A 9% Preferred ($1,000 / share) 1,809 $1,809 1,809 $1,809 562 562 Series B 9% Preferred ($25 / share, $5.00 conversion price) 4 1,595,900 $39,898 1,595,900 $39,898 730,419 18,260 Series C Preferred ($1,000 / share, $2.00 conversion price) 93,000 $93,000 - - - - Common Stock / OP Units 5 11,358,759 $22,717 58,497,605 $116,995 69,939,607 $139,879 Market Value of Equity $157,424 $158,702 $158,701 Total Capitalization $305,058 $322,528 $322,527 1. After giving effect to the exchange of the Series A & B Preferred Stock that closed on July 20, 2015

2. 648,425 warrants were issued in connection with the Senior Non-Convertible Debt, each with a $4.75 exercise price and expiration in

Jan-19 3.

Convertible at lesser of $5.50 or 95% of the offering price for a firm

commitment, underwritten, public Follow-On of common stock

4. 1,987,500 warrants were issued in connection with the Series B Preferred Stock, each with a $5.50 exercise price and expiration in

Apr-19 5.

Assumes a $2.00 stockprice |

NASDAQ: WHLR For Additional Information At the Company: Investor Relations Counsel: The Equity Group Inc. Robin Hanisch Corporate Secretary Robin@whlr.us 757-627-9088 Laura Nguyen Director of Capital Markets Laura@whlr.us 757-627-9088 Terry Downs Associate TDowns@equityny.com 212-836-9615 Adam Prior Senior Vice President APrior@equityny.com 212-836-9606 Think Retail. Think Wheeler.® |